One payment. A fresh start. Real debt relief for the life you deserve.

Register or log in for a FREE personalised assessment. Find your clear, affordable path to financial peace of mind today.

One payment. A fresh start. Real debt relief for the life you deserve.

Register or log in for a FREE personalised assessment. Find your clear, affordable path to financial peace of mind today.

Debt consolidation is taking all your separate debts, like credit cards, store accounts, or loans, and merging them into one. Instead of juggling multiple payments every month, you just have one, often with a lower interest rate. It’s a smart way to simplify your finances and breathe a little easier.

At JustMoney, we understand how overwhelming debt can feel. That’s why our debt consolidation solution is designed to help you take back control of your finances.

Our National Credit Regulator-registered partner helps to:

Register or log in to your JustMoney dashboard. Under “Take control of your debt”, click the “Call Me” button. Your interest in paying your debt will be noted, and a qualified financial adviser will call you to discuss your options. The assessment is non-obligatory and it’s FREE.

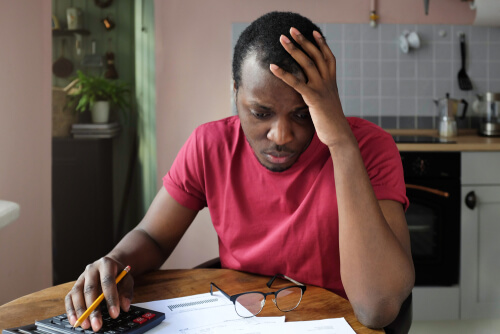

In South Africa today, the average person spends nearly 70% of their take-home pay just to service debt. That’s not just a financial burden, it’s a crisis.

In this kind of environment, debt consolidation offers relief, control, and a real plan forward:

One payment instead of many: No more juggling five different lenders, due dates, and interest rates. You get one monthly payment, often at a lower rate, with a clear end date.

Lower interest equals more cash in your pockets: Unsecured debt in South Africa carries an average interest rate of 23% per annum, but through our consolidation plan, that rate can drop to as low as 3%.

A clear path to freedom: Instead of endless minimum payments, you get a structured plan to become debt-free in 3–5 years. You’ll know exactly when the struggle ends.

Your credit can recover: As you make consistent payments, your credit score improves. That opens doors to better financial opportunities in the future.

Peace of mind: Debt stress affects your sleep, your relationships, and your mental health. Consolidation gives you clarity and control, helping you breathe again.

| Before consolidation | After consolidation (with JustMoney’s partner) |

| Credit card: R25,000 debt (repayment R1,800 per month) Store account: R15,000 debt (repayment R1,300 per month) Personal loan: R40,000 debt (repayment R2,100 per month) Total monthly repayment: R5,200 across three different creditors (more admin and stress) | One lower monthly payment: R3,700 Legal protection: Your assets are protected, and creditors can’t harass you Reduced interest rates: Your debt counsellor negotiates lower rates on your behalf Peace of mind: You have a clear, manageable plan to become debt free |

TIP: Use our budget calculator to check your income versus expenses.

Start your journey to financial wellness

Apply online in minutes, at no cost. Should you qualify, your new plan will have lower instalments, freeing up cash and reducing stress.

See if you qualify – it’s free and won’t affect your credit score. Register.

Debt consolidation might be the right solution for you if:

Explore your debt management options here.

Type of debt | Can it be consolidated? | Notes |

Personal loans | Yes | Most common for debt consolidation plans |

Credit cards | Yes | Combine high-interest cards into lower debt instalments |

Retail store cards | Yes | Game, Edgars, etc. |

Short-term loans | Yes | Must meet minimum balance |

Student loans | Sometimes | Case-by-case basis |

Secured debt (home, car) | No | Can be included in a debt counselling plan but must be up-to-date and paid throughout. |

Discover more tools:

Learn more about DebtBusters, South Africa’s leading and most trusted debt management company.

Debt counselling combines your monthly repayments, leaving you with one instalment per month. Reduced payments and interest amounts will be negotiated with your creditors on your behalf.

Know the difference between debt consolidation and debt counselling, to determine which financial solution is the right one for your needs.

In this article, we consider the difference between having debt and being over indebted, and outline some tips on how to alleviate financial strain.

While you are under debt counselling, creditors are not allowed to contact you, leaving you with a measure of peace while you get your debt back under control.

Navigating the complexities of multiple debts can be daunting, but debt consolidation offers a beacon of financial clarity. As a sought-after strategy for consumers with several debt obligations, debt consolidation not only streamlines repayments but can also pave the way for saving. Dive into our comprehensive articles to unravel the intricacies of debt consolidation, its merits, and how it can be your stepping stone to a more manageable financial future.

Before taking a payment holiday in South Africa, understand the costs, credit score impact, and better alternatives for your situation.

Worried debt consolidation will hurt your credit in South Africa? Learn how it impacts your credit score, card use, and long-term financial health.

Learn whether you qualify for a debt consolidation loan in South Africa. Discover requirements, benefits, and how it can help pay off your debts.

Confused about how debt consolidation loans work? Learn the pros and cons, and the credit score impact in South Africa.

The excitement that comes with the festive season can make you forget that this period is going to pass. You go out of your way to make it memorable for you and your loved ones by splashing out on gifts, and maxing out on groceries via store card credit

The emergence of COVID-19 has dramatically changed our lives. The financial impact has been sweeping and has resulted in massive job losses, business closures and salary cuts.

Food is becoming prohibitively expensive in South Africa. In January, StatsSA released a study showing that food and non-alcoholic beverages are some of the biggest contributors to inflation.

When you start debt consolidation, you will have the opportunity to bundle all your outstanding debts into a single debt. But which debts are you allowed to include in this process?

If you’re struggling to manage your debt and you decide to seek help, you will likely come across the terms “debt counselling” and “debt consolidation”. Although they sound like synonyms, these are two separate...

Join the thousands of South Africans who have used JustMoney to help lower their stress, get out of debt more quickly, and take back control of their finances. Our debt consolidation solution can help you combine debts into manageable, affordable monthly repayments.