Somewhat ironically, each new year immediately launches into the same old news cycle: the WEF meetings at Davos, the State of the Nation (Sona) speech, presentation of the national Budget to Parliament. Those a bit longer in the tooth may feel that it’s all over-hyped, over-reported and over-analysed, “sound and fury, signifying nothing”. Because, invariably, these events don’t become watershed moments, just brief intermissions that change little, if anything at all.

Except this year, I hear you say … well maybe. This year, Cyril Ramaphosa becoming president has brought a real edge to proceedings, an anticipation as to who will do the talking, to what agenda, and with what effect. This year, there is the expectation that we will address our problems with real-world solutions not monotone platitudes, and that this year our stock market will be sure to react to these occasions.

Our positive reception at the World Economic Forum, and the continuing rand strength, is an indication of how much the international community wants us to succeed. But it could all also just collapse under the realisation that nothing will change, or that our economic challenges will not be solved by new leadership, even with the best of intentions.

Although events like Sona and the Budget speech in Parliament have an effect on investor sentiment, they should not interfere with your retirement planning. If your investment plan is to wait for calmer waters before getting into shares, chances are you’ll never get onboard. It also means you probably won’t reach your financial goals.

Many people avoid the stock market because it can seem like a crap-shoot. Contrary to the many ‘informed’ opinions out there, there really is no saying where it will go next. It’s a relentless up and down, promising either a quick buck, or a whole lot of remorse. No wonder so many industry terms have their origin in gambling.

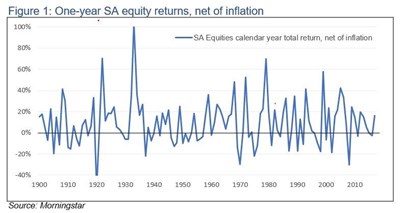

That’s also what Figure 1 suggests. It shows the annual return from the South African share market (net of inflation) since 1900. There is no pattern in these returns – they are entirely random, which means they are impossible to predict or manage.

Every so often you get a down year that will leave you wistful, or a full-on market crash, which will prompt morose thoughts about how you could have squandered that money in more hedonistic fashion.

Fittingly, the graph resembles a sound wave because much of what drives these annual moves is just noise – market chatter, economic data, company results, central bank policies, local politics and geopolitics, anything that might shed light on the size and certainty of the market’s future cashflows.

The daily news flow affects the ebb and flow of investor sentiment and expectations. Regrettably, a lot of people are put off by the resultant volatility, and let it influence how they invest. They choose the money-in-the bank option because it comes with an (almost) guaranteed return, and a good night’s sleep.

South Africa has always been a noisy place, but recently we seemed to reach a crescendo. We were not so much lurching from one crisis to another as layering them on thick and fast, one on top of the other, unresolved, creating an ‘Arc de Crise’, a monument to mismanagement. The cornerstones were laid decades ago, but the building work was more frantic than ever.

There was former president Jacob Zuma’s “Apres moi, le deluge” approach to statesmanship, the plunder of our limited resources under his watch and the undignified struggle to get him off the throne so that the country could clean up his mess.

There is also the issue of corporate complicity in our state’s capture, soiling our international reputation for governance.

There’s the ruling party’s indulgence of our failing and bankrupt state-owned enterprises, the annual handwringing over South African Airways (SAA), Eskom, the South African Broadcasting Corporation (SABC), the Passenger Rail Agency of South Africa (Prasa) and the South African National Roads Agency (Sanral) and the refusal to put these assets into accountable – that is, private – hands.

There is the deteriorating health of our public finances, the shrinking tax revenues, the widening budget deficit, the growing debt pile, the prospect of an ever-increasing tax burden. Moody’s’ hands are itching to drop the guillotine on our investment-grade credit rating.

Add in the very public failures of Cape Town’s water management and Steinhoff’s accountants (to mention just two) and it becomes a daily battle royal for the front page. It’s not exactly a feel-good environment that encourages investing in the JSE.

That’s undeniably true if you need your money sooner rather than later. If nothing else, the one-year return graph confirms that the share market is no place for a short-term investment.

But let’s extend that time horizon to, say, five years. Is cash still safer than shares then? And by safer we mean, does cash outperform equities occasionally – as is the case on a one-year view – and does it present less downside risk during difficult times?

The answer to both these questions is ‘no’.

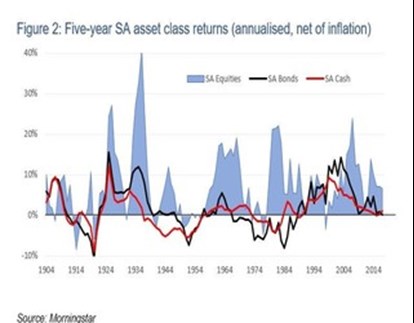

Figure 2 tracks the 5-year annualised return (net of inflation) for South African (SA) equities, bonds and cash since 1900. Two things stand out. First, the annualised real share market return over five years was almost never negative. It’s happened only once over the last 40 years.

Second, you are hardly ever better off holding cash (or government bonds) rather than equities. The one stand-out exception was around the turn of the millennium, when a series of bursting market bubbles, economic crises and currency collapses pushed our interest rates into the stratosphere. Other, much briefer, periods overlap with World War 1 (WW1), the Great Depression and the high-inflation Seventies.

More remarkable are the periods when it didn’t happen despite the negative backdrop, such as World War 2 (WW2), the 1980s sanction era, or the Global Financial Crisis around 2008.

The point is, it can happen, but it rarely does. From a historical perspective, the probabilities massively favour equities. If you are investing for longer than five years, you can have a high degree of confidence that you’ll do better with an index fund replicating the broad share market than with your savings account.

The longer you plan to invest, the higher your comfort level should be. Over 30 years, there hasn’t been a single instance when you would have smiled holding cash over equities (Figure 3). Rarely has it been close, even over the worst of times. In fact, the highest return from cash over any such period (3,7%) is still below the worst return from equities (4% pa).

Just as instructive is the difference in the long-term compound real return of these two asset classes: 7,3% per annum for SA equities, 1% per annum for cash. To put that into perspective, R1 growing at 7,3% per annum turns into R8,30 after 30 years, R1 growing at 1% per annum, just R1,35. One will help you fund a decent retirement if you save adequately and consistently; the other will lead you to the poor house even if you save twice as much.

Of course, future returns are uncertain and not guaranteed, but it would take a brave person to bet against a 120-year track record.

Yes, we are in a mire, with respect to some of the issues listed above. But understand that these are the same feelings investors had about this place in the Seventies, Eighties, Nineties and Noughties. Every time, we overcame our problems, and the feelings passed. And that’s the point: we are talking about temporary negative emotions stirred by the news cycle. As sickened as we all are about the events of the past few years, this comes from our sense of propriety, much more than from how these stories impacted us personally.

It unsettles us today, but tomorrow it’s in the trash, out of sight and, within a day or two, out of mind. Pick up a paper from a year ago, and you’ll realise that almost none of it mattered. And while you dithered, the stock market went up another 20%.

The thing to do is to see the media for what it is – an entertainment business – and the fear mongers for what they are – people trying to sell you something. Then invest, according to your time frame, and not how crappy they made you feel today.